The mutual fund return number: choose your reality wisely

Three metrics – CAGR, XIRR, Rolling Returns – tell three completely different stories about the same investment. Here's which one you should actually be using.

By Kshitij Jain

Every mutual fund advertisement you've seen quotes a CAGR. The Nifty 50 returned 13.2% CAGR over the last 10 years. Fund X delivered 18% over 5 years. These numbers are real but also almost completely useless for understanding what you actually earned.

Some mutual funds might surprise you with their skyrocketing CAGR of 30–40% but it doesn't tell the true picture. What's missing is time – specifically, your time in the market, and when your money entered.

The three measures: CAGR, XIRR, Rolling Returns.

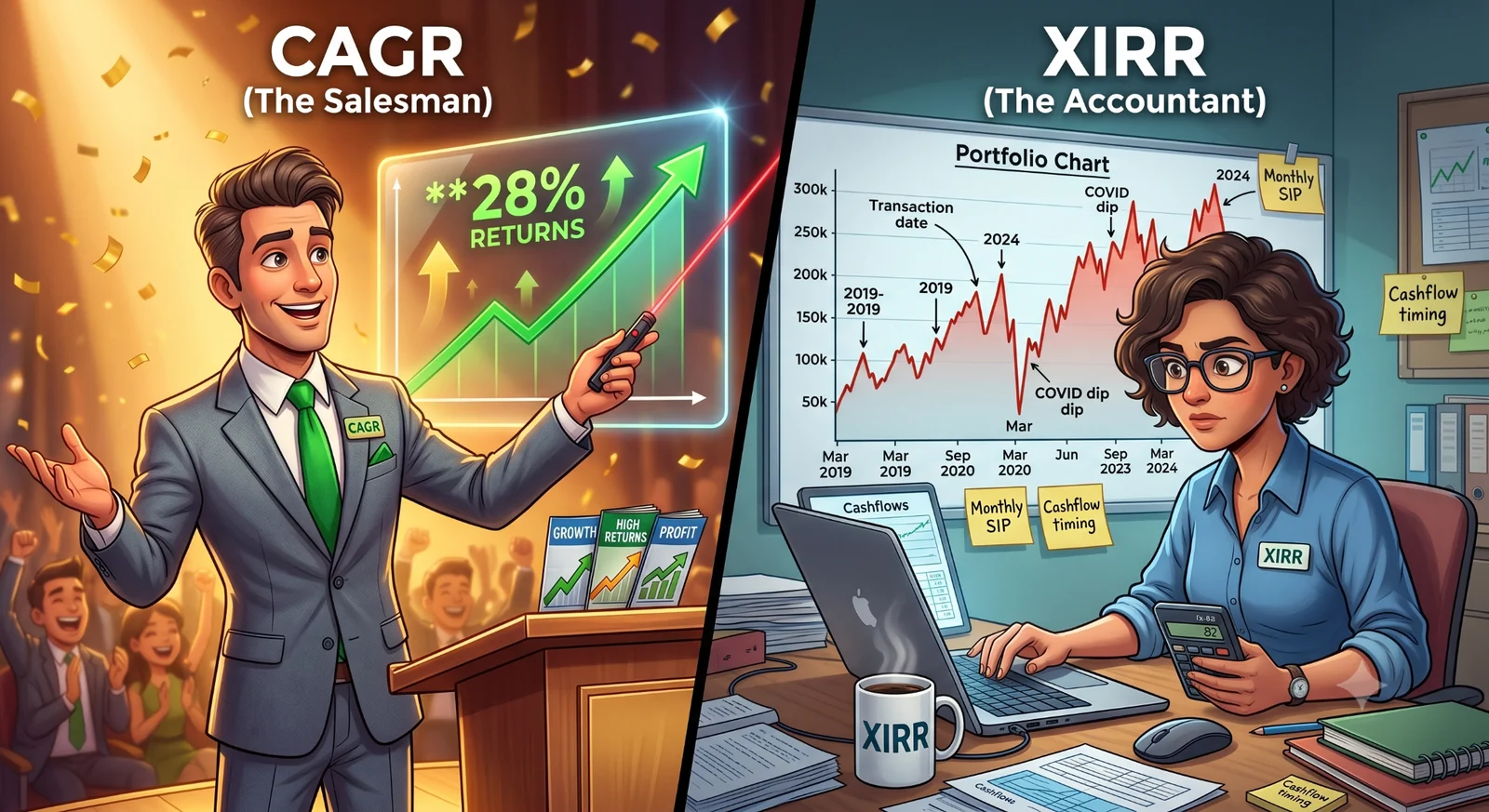

CAGR: the salesman

CAGR (Compound Annual Growth Rate) answers a clean hypothetical: if ₹1 lakh grew to ₹2.5 lakh in 7 years, what constant annual rate explains that?

The formula: (End Value / Start Value)^(1/n) − 1.

CAGR does not consider the timing and amount of any cash flows that may have occurred during the investment period. So it works perfectly for a lump sum sitting untouched. But the average Indian investor doesn't invest in lump sums – they do SIPs. And for SIP investors, CAGR is measuring someone else's journey.

The problem: the Nifty 50 fell roughly 38% between January and March 2020, then recovered to all-time highs by late 2020. A fund house quoting 5-year CAGR starting from that March (after the fall) would show CAGR north of 35%. The same fund, measured from January 2020, would show ~13%. Same fund. Same assets. Different window.

XIRR: the accountant

XIRR takes into account the timing and amount of all cash flows during the investment period. It is particularly useful for measuring the performance of mutual funds that involve periodic investments or redemptions, such as SIP investments. It considers each instalment in an SIP a new investment, along with the total time for which it was invested.

If you invested in a 10-year monthly SIP, your first instalment was invested for 10 years, second for 9 years and 11 months, and so on. So each SIP amount is compounded for a different period. XIRR calculates the CAGR of each SIP instalment and then adds all these together to give one overall compounded rate.

| CAGR | XIRR | |

|---|---|---|

| What it measures | Annualised growth between a start and end value | Annualised return accounting for exact timing and size of every cashflow |

| Best suited for | Lump sum | SIPs & staggered flows |

| Cashflow treatment | Ignores intermediate flows entirely | Fully incorporates timing, size and frequency |

| Market timing sensitivity | High – start/end point dependent | Low – smooths SIP timing |

| Complexity | Simple formula, single calculation | Requires all transaction dates and amounts; iterative solver |

| What it shows you | How much did an investment grow per year on average? | What was your real return experience as an investor? |

| Best use case | Comparing long-term wealth growth of lump sum investments across funds | Reviewing your personal SIP portfolio performance |

| Key limitation | Easily gamed by cherry-picking start and end dates | Needs complete, accurate cashflow data – messy if records are incomplete |

| What it can't tell you | Anything about volatility or the journey in between | Whether the fund itself is consistently good, or you just got lucky with timing |

| How fund houses use it | Primary marketing metric; window is usually cherry-picked | Rarely quoted; requires investor-specific data |

Rolling returns: the honest version of history

Rolling returns ask one question: what would you have earned if you had started investing on any random day in the past?

Instead of picking one start date and one end date – which is what CAGR does – rolling returns run that same calculation for every possible start date across a long period.

Say you want to know how a fund performed over any 5-year stretch between 2015 and 2025. Rolling returns calculate the 5-year CAGR starting January 2015, then February 2015, then March 2015, all the way to January 2020 (with the last possible 5-year window ending in 2025). You end up with hundreds of return figures instead of one. That spread – the best case, the worst case, the median – is what rolling returns show you.

The point isn't precision. It's honesty. A fund can flash a 25% CAGR by starting its window after the COVID crash of March 2020 and ending at the 2025 peak. Rolling returns make that trick impossible, you're seeing all the windows at once, including the ones where someone started a SIP right before a crash.

Nifty 50 historical rolling returns (1991–2026)

| Holding period | Mean CAGR | Median CAGR | Worst window | Best window | Negative periods |

|---|---|---|---|---|---|

| 1 year | 17.4% | 8.4% | −47.1% | +134.1% | 9 out of 35 |

| 3 years | 12.2% | 9.6% | −13.7% | +52.6% | 4 out of 33 |

| 5 years | 11.3% | 11.5% | −6.2% | +37.5% | 1 out of 31 |

| 7 years | 11.2% | 11.3% | 0.02% | +24.5% | 0 out of 29 |

| 10 years | 11.3% | 11.9% | 2.5% | +18.3% | 0 out of 26 |

| 15 years | 11.8% | 11.9% | 4.9% | +16.5% | 0 out of 21 |

Source: BMS Money

Notice what longer holding periods do: they compress the worst case dramatically while keeping the median stable – the mathematical argument for staying invested longer.

The reason is compounding arithmetic. A bad year needs time to recover. Over one or two years, there may not be enough time for that recovery to fully materialise. But over 7 or 10 years, the market has had multiple cycles to mean-revert.

The crashes that devastate short-term holders – 2001, 2008, 2020, 2026 – become speed bumps in a longer return series, their damage diluted across years of compounding that preceded and followed them.

So which number should you use?

To review a portfolio meaningfully, you need to look beyond a single return number to understand the performance of the portfolio from different angles.

A simple decision rule:

- Comparing two funds? Use CAGR, but make sure the windows are identical.

- Reviewing your own SIP portfolio? Use XIRR, it's the only number that reflects your actual cashflow reality.

- Deciding whether to invest in a fund? Use rolling returns. Ask: in what % of 5-year windows did this fund beat its benchmark?

The reason fund houses prefer CAGR isn't accidental, it's the most flattering number in a rising market, requires no knowledge of when you invested, and is easy to cherry-pick by window. XIRR requires your actual transaction data. Rolling returns require work. Neither fits a 30-second advertisement.

Tools to try

Run the numbers yourself.

Free calculators that go with this issue. Built for Indian rules (rupees, inflation, tax regime).

- SIP Calculator – Monthly Mutual Fund Returns India

Estimate the future value of a monthly mutual-fund SIP in India. Plug in your SIP amount, expected return (8–12% historical equity), and horizon to see the corpus and gain split.

- Mutual Fund Returns Calculator – SIP + Lumpsum India

Project combined returns from a mutual-fund SIP, lumpsum, and one-time top-ups in one calculator. Built for Indian equity, debt, hybrid, and ELSS funds with realistic return assumptions.

- Lumpsum Calculator – One-time Investment Returns India

Estimate the future value of a one-time mutual-fund or fixed-income lumpsum in India. Enter principal, expected annual return, and horizon to see the corpus, total gain, and compounding split.

- IRR Calculator – Internal Rate of Return on Cash Flows

Compute the Internal Rate of Return on any series of uneven cash flows – the right way to compare investments with irregular contributions or payouts, like real estate, PMS, or business equity.