Trading the Monsoon: For the First Time in India

India just turned rainfall into a tradable asset – right as the monsoon went missing.

A derivative is an instrument whose pricing is based on an underlying asset. Here, the underlying asset is not a stock or a commodity. It is rain.

A weather derivative pays out based on a measurable atmospheric variable – rainfall, temperature, wind. RAINMUMBAI’s index updates daily from IMD stations at Santacruz and Colaba.

Energy utilities, airlines, and agriculture companies in the West have used these for decades. India is late – but the timing is slightly unfortunate.

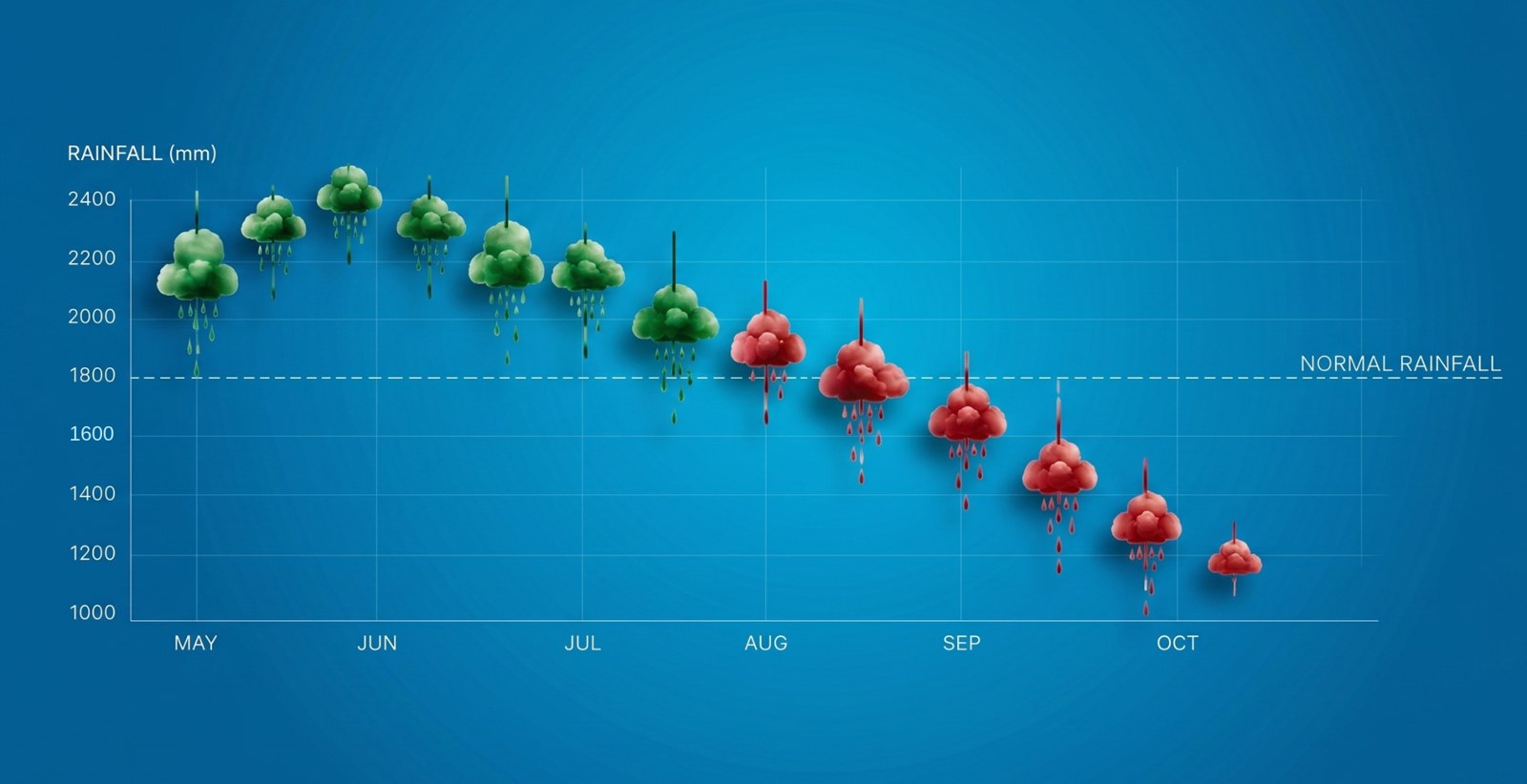

As of June 16 – two weeks after launch – India’s monsoon deficit stands at 35% nationwide, with central India 63% below normal. Rain clouds have yet to reach Mumbai. NOAA has placed the odds of a very strong El Niño by winter at 63%.

The monsoon is a macro asset

In India, a weak monsoon is not a weather story. It is a rural income story, which is a consumption story, which is a CPI story, which is an RBI policy story.

Agriculture is 18% of GVA and employs nearly half the workforce. The Kharif season – rice, pulses, oilseeds, cotton – depends almost entirely on the southwest monsoon.

The 2026 picture has a specific edge: IMD’s most pessimistic pre-season forecast since 2015, a 35% June deficit – and crucially, deficits in June are unusual. The damage in most El Niño years arrives in July and August. Analysts waiting for July data to revise earnings models may already be behind.

The real risk: basis risk

RAINMUMBAI is a genuine breakthrough. But it has one catch.

The contract pays out based on what two IMD stations in Mumbai record – not based on what actually happened to your business.

Picture a normal season at those stations while your warehouse in Andheri floods. The index recorded normal rainfall, so there is no payout. Your loss was real; the index didn’t see it. That gap is called basis risk.

It shows up in two ways:

This isn’t a flaw unique to RAINMUMBAI. That’s the tradeoff. Speed and simplicity in exchange for precision.

This works best for businesses whose losses move with Mumbai’s rainfall overall – logistics, utilities, large insurers.

The fix is more stations. Contracts tied to local gauges, closer to where the exposure actually is.

The bottom line

Weather has always priced into Indian markets. RAINMUMBAI is the beginning of weather becoming a proactively priced variable: hedged before the damage is counted, not after.

Mumbai is the proof of concept. Agricultural districts are the logical next step – where the stakes are higher and the basis risk, with local gauges, is far lower.

India has absorbed $180 billion in weather-related losses over 30 years. Until now, there was no market to hedge any of it.

The monsoon is no longer just a prayer. It is, finally, a contract – and right now, with a 35% deficit and a Super El Niño building, the launch comes with risks.

Tools to try

Run the numbers yourself.

Free calculators that go with this issue. Built for Indian rules (rupees, inflation, tax regime).

← Newer issue

Is PMS an Upgrade to Mutual Funds – Or Just a More Expensive One?

Older issue →

Forget the Rockets. Look at What Google Is Paying SpaceX For.

Also worth reading

12 June 2026

Forget the Rockets. Look at What Google Is Paying SpaceX For.

Everyone knows SpaceX makes rockets. Almost nobody knows Google pays it $920 million a month – and Anthropic $1.25 billion – to run AI. Inside the IPO that is really an infrastructure, and xAI, bet.

29 May 2026

Betting on IPL: The Game Behind the Game

IPL viewership dropped 26% the year India banned real-money fantasy gaming. The 250 million users didn't go home – they went underground, to WhatsApp groups and prediction markets. Here's what India broke when it banned Dream11.