Betting on IPL: The Game Behind the Game

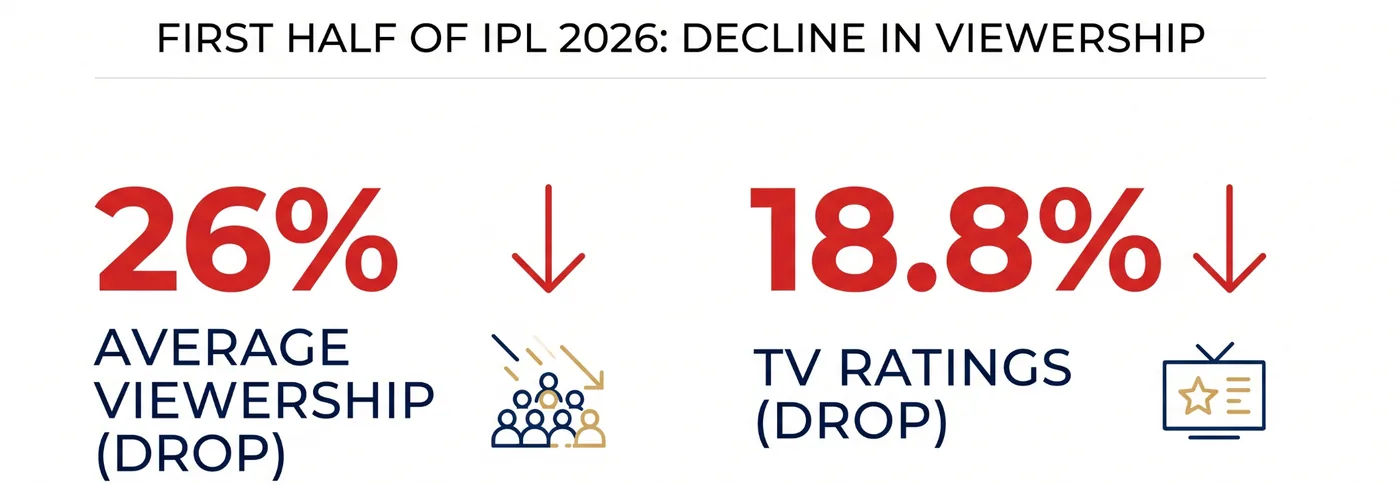

IPL viewership dropped 26% the year India banned real-money fantasy gaming. The 250 million users didn't go home – they went underground, to WhatsApp groups and prediction markets. Here's what India broke when it banned Dream11.

By Harsh Soni

It is a Tuesday night in April. Chinnaswamy is packed. Men in red jerseys everywhere – on the stands, on the screen, on the couch at home. Virat Kohli has just walked in to bat and the volume in every living room in the country has gone up two notches.

Except, this year, the audience watching has decreased by 26%. In a country where cricket isn't just a sport but a shared national obsession, that number is jarring.

The explanations are familiar: cricket fatigue, high-scoring games that have become predictable. All probably true to some degree.

But there's one more that stands out from the rest – the one whose timing lines up too precisely to ignore – the real-money gaming ban.

Last August, Parliament passed the Online Gaming Act and, almost overnight, wiped out Dream11, My11Circle and every fantasy cricket platform in India.

What the viewership data is actually telling us isn't that cricket has gotten boring. It's that for crores of Indians, watching and wagering were never really two separate activities. The match was the interface. The stake was the reason to stay.

The big ban

The Online Gaming Act banned the app, Dream11, from running its real-money game model. Here's what happened next.

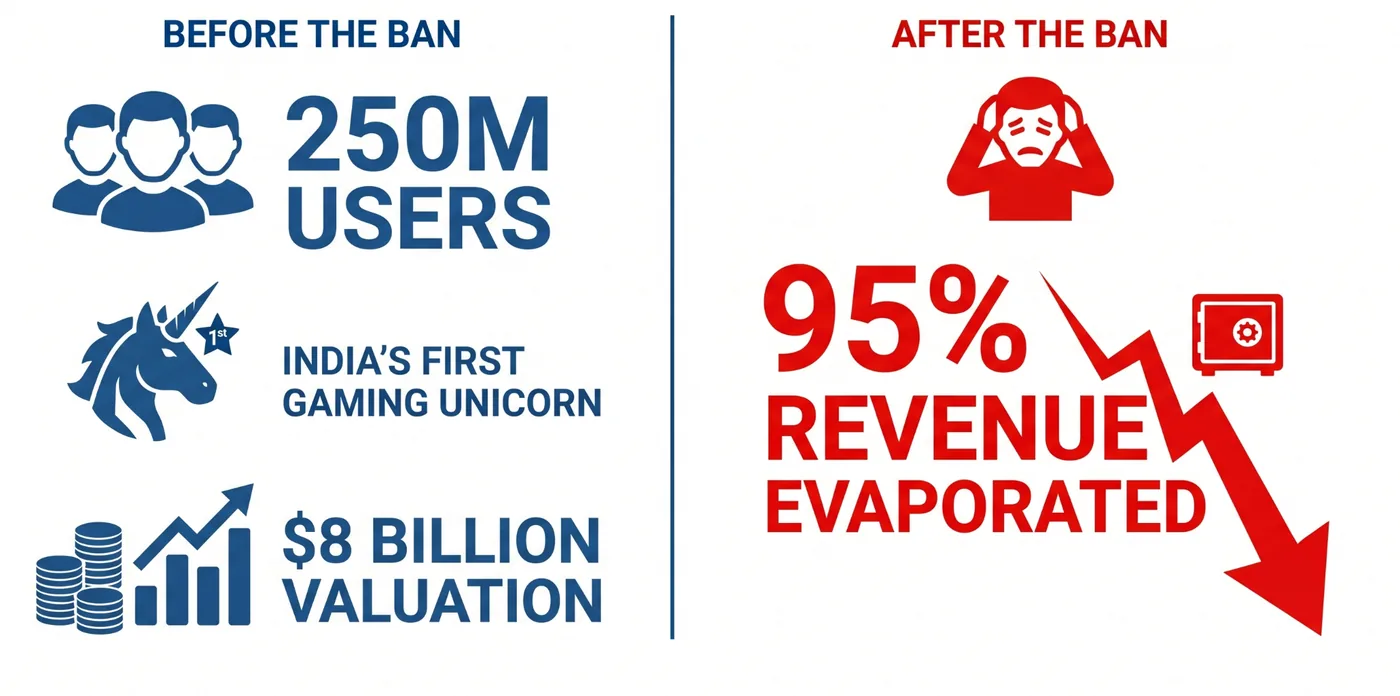

Dream11's legal defence was elegant: fantasy cricket is judgment, not luck. You study form, read pitch conditions, analyse matchups. A "game of skill" they called it. After the ban, the platform shifted to a free-to-play model.

The 250 million users it left behind – the single largest concentrated pool of cricket intelligence on earth – didn't stop having opinions. They just lost the legal place to act on them.

And that is where the story gets darker.

The billion-dollar illegal industry

As of March 2026, the government has blocked 300 websites and apps, making the total restricted websites nearly 8,400 in number.

The newer platforms have made even that look silly.

Platforms like 99 Exchange and 11xplay now have no website to block, no accounts to freeze. You join through a WhatsApp group. Money moves through UPI – person to person, the same as splitting a dinner bill.

India banned the legal version. The dangerous one upgraded.

The predictive market playbook

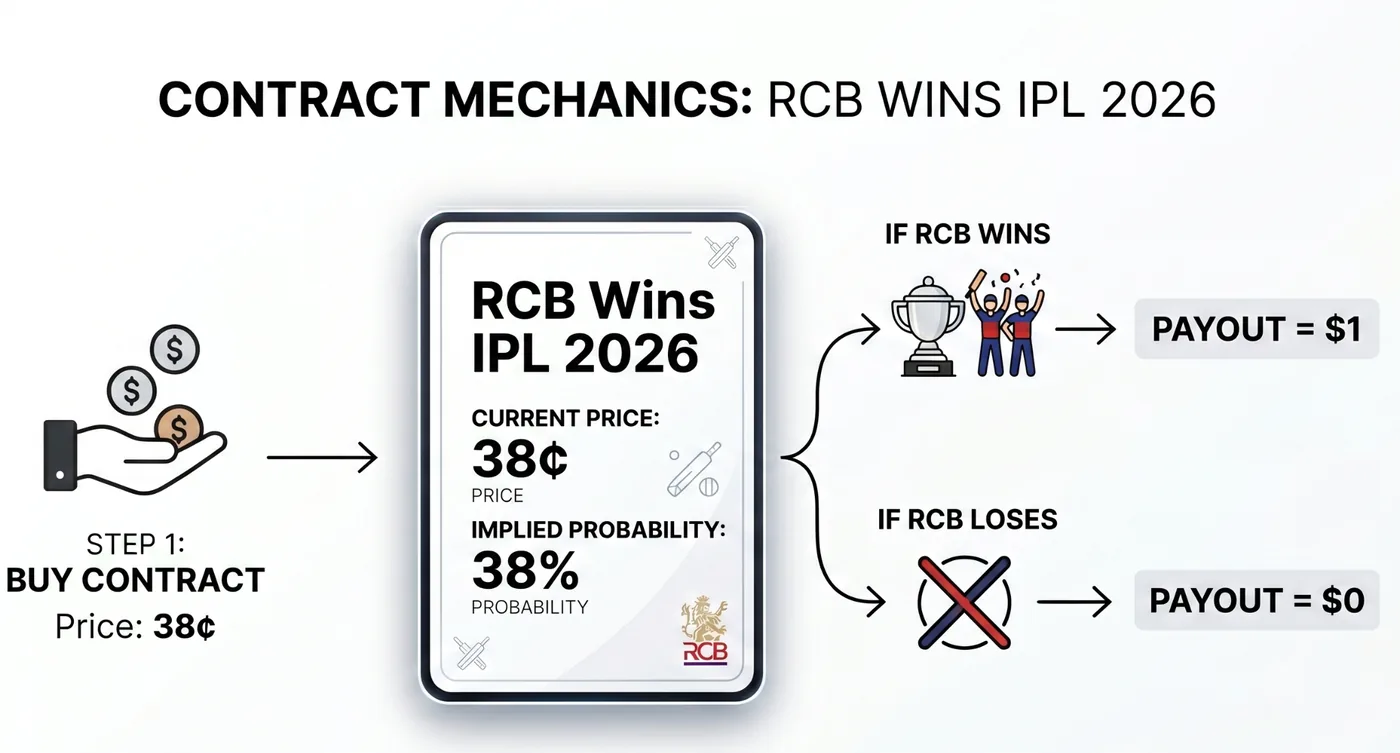

On predictive market platforms like Polymarket, IPL outcomes are actively traded.

Think of it like a stock, but instead of a company, you're buying a share in an outcome. The diagram below shows how it works.

That price isn't set by an algorithm or an analyst. It's set by every buyer and seller on the platform – putting real money behind their real beliefs.

The market is, in effect, a live probability machine built out of human judgment and financial stakes.

This IPL season itself, millions of dollars have been traded on the single question of who wins the 2026 trophy.

The case against such markets: the unfair advantage

Zoom out from the enforcement directive for a moment, because there is a more interesting question buried in here.

The intellectual case for prediction markets rests on an idea from the economist Friedrich Hayek: no government or expert panel can gather all the information dispersed across millions of individual minds.

Markets do it automatically – the fan in Bangalore who has watched every RCB match carries knowledge no analyst can replicate, and every transaction expresses that knowledge as a price signal.

It sounds democratic. The crowd's collective wisdom, priced in real time. But the reality is different.

The theory assumes participants are diverse, independent, and rational. Cricket fans, however, are highly emotional and irrational. When MS Dhoni walks to the crease, prices shift in CSK's favour regardless of what the run-rate says – the market processes sentiment alongside information, and cannot always tell them apart.

But the bigger problem is information asymmetry. In equity markets, acting on privileged information is insider trading. It is a crime. In prediction markets, the same dynamic plays out with no legal framework to contain it.

In December 2025, a US soldier began accumulating contracts on Polymarket predicting Maduro's removal. On January 3, 2026, the US military captured him. The trader collected $400,000.

Weeks later, $2.4 million in contracts predicted US strikes on Iran – placed just before they occurred. Both events flagged as potential trades on classified information.

In an IPL context, that someone is the physio who knows a bowler's shoulder isn't right, or the franchise insider who knows a star will be rested. The fan who has watched every match since childhood thinks he has an edge. He is almost certainly trading against someone who already knows the answer.

The market looks like a level playing field. It isn't.

The case for such markets: the legal safe bet

In May 2026, MeitY issued a blocking order against Polymarket. Despite that, the platform was still letting Indian users sign up after the order went out. The government declared them dark. They stayed lit.

The rest of the world ran a different experiment.

The UK legalised sports betting in 2005 – it is now a £4 billion industry. In the US, Kalshi had to sue its own regulator to establish that a prediction market is a financial instrument, not a gambling product. It won. Kalshi is now valued at $22 billion.

The consistent finding: legalisation doesn't create new gamblers – it moves existing ones from unprotected platforms to licensed ones, where they have rights and the government collects tax. India is losing an estimated ₹27,000 crore annually in taxes to a market it cannot see.

Would legalisation fix everything? Probably not. Insiders would still have an edge. The Dhoni-effect bettors would still be irrational.

But it would bring the activity into the open – where consumer protections apply, disputes have a resolution mechanism, and the 70% who lose money at least lose it somewhere accountable, with oversight, protection, and receipts.

To do that, India still needs a far more sophisticated system.

The most informed cricket market in the world is potentially operating in the dark. And the question of whether to legalise it still persists.

← Newer issue

You can't lose with SIPs: if you stick around long enough

Older issue →

Flipkart's IPO has been ‘Coming Soon’ since 2019

Also worth reading

29 May 2026

You can't lose with SIPs: if you stick around long enough

Across 29 years of Indian equity market history and 120 diversified funds, no 10-year SIP investor has ever ended in the red. Not low probability – zero. The maths is straightforward; the behaviour is the hard part.

21 May 2026

Flipkart's IPO has been ‘Coming Soon’ since 2019

Flipkart's IPO has been deferred, again. Here's why Walmart hit pause, what the numbers actually say, and what it tells us about the state of India's IPO market in 2026.